Last updated: 06.03.2026 . Author: ploan.ph

Pag-IBIG MP2 is a voluntary savings and investment program offered by the Philippine government through the Pag-IBIG Fund. It is designed for Pag-IBIG members who want to grow their money faster than in the regular Pag-IBIG savings. It is a government-backed savings program that offers high interest rates (up to 7% or more) with tax-free benefits.

Pag-IBIG MP2 (Modified Pag-IBIG II) Savings Program is a special, optional savings facility with a fixed 5-year maturity period for current and former Pag-IBIG Fund members. It allows members to save at least PHP 500 and earn higher, tax-free dividends than the regular Pag-IBIG savings, with earnings guaranteed by the Philippine government.

The Pag-IBIG MP2 Savings Program isn't just another savings account; it's a government-backed investment vehicle designed to supercharge your financial growth. Here's why it's catching the attention of savvy Filipino savers:

If a single payment exceeds ₱500,000, it must typically be made through a manager’s check or bank check.

Members can contribute:

There is no required contribution schedule, so participants can save according to their financial capacity.

The MP2 program has a fixed maturity period of 5 years starting from the date of the first contribution.

At the end of the five-year term, members can:

If the savings are not withdrawn after maturity, the funds may stop earning MP2 dividends and instead earn the regular Pag-IBIG savings rate.

The program offers flexible contributions:

This flexibility makes MP2 suitable for people with irregular income or those who want to invest extra money such as bonuses or savings.

Normally, MP2 savings can be withdrawn after the 5-year maturity period, at which point members receive both their contributions and all earned dividends.

Early withdrawal may be allowed in special situations such as:

If the account is closed before maturity without a valid reason, the member may lose part of the earned dividends.

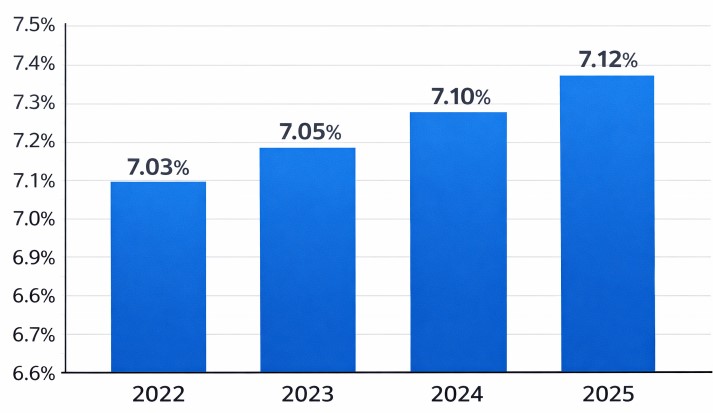

MP2 isn't comparable to a traditional bank deposit since it doesn't accrue interest in the same manner. Instead, Pag-IBIG refers to MP2 returns as "dividends," determined annually based on the fund's net income following approval by its Board of Trustees. This makes the dividend rate variable - while currently at 7.12%, this figure represents just the most recent declaration and offers no guarantee for subsequent years. Future rates will fluctuate according to Pag-IBIG's performance. To estimate potential earnings, simply multiply the declared rate by the amount held in your MP2 account throughout the year, with longer-term deposits yielding greater benefits.

In 2025, Pag-IBIG announced a dividend rate of 7.12% under the MP2 program, marking an increase from the previous year's rate of 7.10%. The fund also declared a record-high total dividend payout of ₱64.34 billion for the year.

While MP2 is considered one of the most popular government savings programs in the Philippines, there are a few important considerations.

The program is open to active Pag-IBIG members and former members with a source of income or pension who have at least 24 months of Pag-IBIG contributions.

This makes MP2 popular among employees, freelancers, and overseas Filipino workers who want a low-risk, government-backed way to grow their savings in the Philippines.

If you are a new to Pag-IBIG, sign up for regular membership and dive into MP2.

Start your MP2 journey with just ₱500.

Yes, under specific circumstances like medical emergencies or permanent relocation.

The returns of Pag-IBIG MP2 depends on the financial activity of the Pag-IBIG fund and can range from 6% to 7.5% per year (including annual interest accrual). Your earnings come from at least 70% of Pag-IBIG's annual net income. In 2024, savers enjoyed a 7.10% dividend rate and in 2025 - 7.12%.

Choose between annual payouts or a lump sum after 5 years.

Absolutely! Diversify your savings strategy with multiple accounts.

Very safe. Pag-IBIG invests primarily in housing finance and government securities, minimizing risk.

Interest |

Loan amount |

Term |

Borrower age |

SEC registered |

||

|---|---|---|---|---|---|---|

|

|

from 0%

|

₱1,000 — ₱50,000

|

up to 12 months

|

20 — 70 years

|

SEC Registration No. CS201908275 SEC Certificate of Authority No. 2990

|

|

|

|

APR 143% per year

|

₱1,000 — ₱20,000

|

from 61 to 183 days

|

22 — 70 years

|

Registration № CS201726430, CA №1181

|

|

|

|

APR 145%

|

₱500 — ₱20,000

|

from 3 to 6 months

|

22+ years

|

SEC Registration number: CS201953O73., Certificate of Authority №1254

|

|