Last updated: 01.06.2026 . Author: ploan.ph

Table of Contents

Table of ContentsA Pag-IBIG loan is a loan program offered by the Home Development Mutual Fund, better known as Pag-IBIG Fund. It is available to qualified Pag-IBIG members who meet the required savings, contribution, document, and account conditions.

There are different types of Pag-IBIG loans:

The most common Pag-IBIG cash loan is the Multi-Purpose Loan. This is the loan many Filipinos mean when they say “Pag-IBIG salary loan,” although the official name is Multi-Purpose Loan.

The Pag-IBIG Multi-Purpose Loan is a short-term cash loan for qualified members. It is designed for personal financial needs, such as:

After the 2025 update, qualified Pag-IBIG members may borrow up to 90% of their total Pag-IBIG Regular Savings, and the minimum contribution requirement for the enhanced MPL was reduced to 12 monthly savings. The changes started on May 16, 2025.

Your actual loan amount is still subject to Pag-IBIG assessment, your savings record, your existing loans, and your account status.

.jpg)

The Pag-IBIG Calamity Loan is for qualified members who live or work in areas officially declared under a state of calamity. It is commonly used after typhoons, floods, earthquakes, volcanic activity, and other disasters.

This loan is different from the Multi-Purpose Loan. It has its own application purpose and eligibility rules. If you are applying because your area was affected by a calamity, check the specific Pag-IBIG Calamity Loan requirements before filing.

More about Pag-IBIG Calamity Loan

.jpg)

The Pag-IBIG Housing Loan is for home-related financing. It may be used for:

This is a long-term loan and should not be confused with the Multi-Purpose Loan. Housing Loan applications require more documents and go through a separate evaluation process.

More about Pag-IBIG Housing Loan

.jpg)

Pag-IBIG also has special loan programs, including health and education-related programs. The 2025 loan enhancement also covered Health and Education Loan Programs, according to government reports on the Pag-IBIG update.

Before applying, always check which loan type matches your actual need. Choosing the wrong loan type can delay your application.

| Item | Details |

|---|---|

| Official loan name | Pag-IBIG Multi-Purpose Loan |

| Common user term | Pag-IBIG salary loan, Pag-IBIG cash loan |

| Best for | Personal expenses, bills, tuition, medical needs, minor repairs, emergency cash needs |

| Loanable amount | Up to 90% of total Pag-IBIG Regular Savings, subject to assessment |

| Contribution requirement | At least 12 monthly savings under the 2025 enhanced MPL rules |

| Repayment options | 1, 2, or 3 years under the enhanced program |

| Online application | Available through Virtual Pag-IBIG for eligible members |

| Status check | Available through Virtual Pag-IBIG Loan Status Verification |

| Main reason for delay | Incomplete documents, account mismatch, contribution issue, employer verification issue, or existing loan problem |

Older articles may still mention 80% loan entitlement or 24 monthly savings. These were previous MPL conditions. For 2026 content, the article should reflect the 2025 update but still advise readers to check Pag-IBIG’s latest official rules before applying.

To apply for a Pag-IBIG Multi-Purpose Loan, you generally need to be a qualified Pag-IBIG member with enough regular savings and an active account record.

A member may file for MPL if they have made at least 12 monthly membership savings, according to the updated MPL application form.

In practice, Pag-IBIG will also check whether:

If you are employed, your employer may need to sign or validate parts of your application. If you are self-employed, a voluntary member, or an OFW, you may need to provide documents that prove your income and identity.

For online short-term loan application through Virtual Pag-IBIG, the listed requirements include:

The loan application form must contain the required information and signatures. For employed members, the form may also need the employer’s signature and the signatures of two witnesses.

Prepare the following before applying:

If you are employed, prepare:

Before applying, check with your HR or payroll department. Some employers process or validate Pag-IBIG loan applications through employer-assisted filing.

If you are self-employed, prepare:

Self-employed members should make sure their contributions are updated and properly posted.

OFWs may also apply if they meet Pag-IBIG eligibility rules. Prepare:

OFWs should check Virtual Pag-IBIG or contact Pag-IBIG directly if they cannot visit a branch in the Philippines.

For the Multi-Purpose Loan, the maximum amount is based on your total Pag-IBIG Regular Savings.

Your Regular Savings include:

Under the enhanced MPL rules announced in 2025, qualified members may borrow up to 90% of total Regular Savings.

Example:

If your total Pag-IBIG Regular Savings is ₱20,000, your maximum loanable amount may be up to ₱18,000 before possible deductions.

However, this does not mean every applicant will automatically receive the full amount. Pag-IBIG may deduct unpaid balances, penalties, or other obligations. Your final proceeds may be lower if you have an existing Pag-IBIG loan.

For the enhanced Multi-Purpose Loan, reports on the 2025 update state that the monthly interest rate remained at 1.4583%. The enhanced program also introduced more repayment options, including 1-year, 2-year, and 3-year terms.

In simple terms:

Before borrowing, estimate whether the monthly amortization fits your budget. Do not borrow the maximum amount just because you are qualified for it.

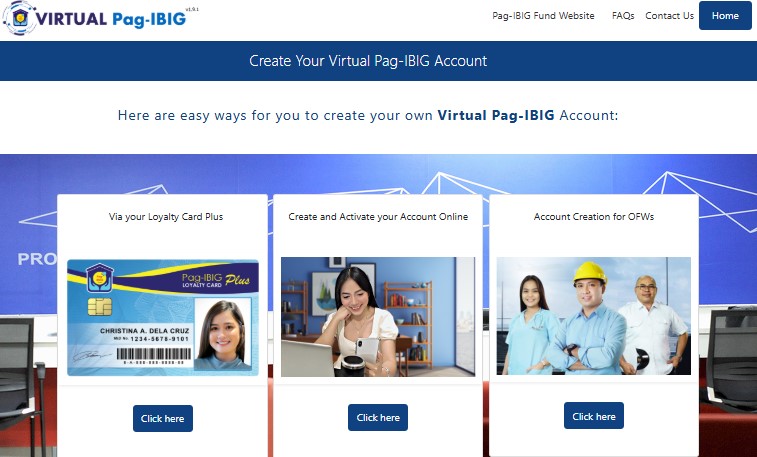

Many members can apply through Virtual Pag-IBIG. The official Virtual Pag-IBIG loan page allows users to apply for and manage loans, including short-term loans and housing loans.

Before filing, check:

You may need a Virtual Pag-IBIG account to view your savings and loan records online.

Select the loan that matches your need:

Choosing the wrong loan type can cause delays.

Prepare clear scanned copies or photos of:

For online short-term loan applications, Virtual Pag-IBIG lists the application form, one valid ID, cash card, and selfie photo as required items.

Access Virtual Pag-IBIG and choose the loan application service. You may be asked to log in, validate your MID, provide contact details, and upload documents.

Make sure:

A blurred ID, wrong MID number, or missing signature may delay processing.

After submitting, save your reference number or confirmation. Take screenshots if needed.

Processing time may vary depending on:

Avoid relying on a fixed processing time from old blog posts. Pag-IBIG’s actual timeline may vary.

If approved, the loan proceeds may be credited to your accepted disbursement account, such as Loyalty Card Plus or another approved cash card.

Online filing is convenient, but it is not always the best option for every member.

You may apply through your employer or HR if:

You may need to visit a Pag-IBIG branch if:

For many employees, the fastest first step is to ask HR whether the company assists with Pag-IBIG loan filing.

You can check your loan status through Virtual Pag-IBIG Loan Status Verification. The official status verification page lets users select the loan type, including Housing Loan, Multi-Purpose Loan, or Calamity Loan.

To check your status, prepare:

If the status does not update immediately, do not submit multiple applications right away. First check whether your documents were accepted, whether your employer needs to validate anything, or whether Pag-IBIG needs more time to verify your records.

A Pag-IBIG loan is not automatically approved just because you are a member. Applications can be delayed or rejected for several practical reasons.

Common issues include:

Before applying, check your records and documents. Many delays are caused by small errors that could have been corrected before submission.

A Pag-IBIG loan and a private online loan are not the same. Pag-IBIG is usually more suitable for members who can wait for verification and who meet the savings and contribution rules. Private online loans may be faster, but they can also be more expensive.

| Criteria | Pag-IBIG Loan | Private Online Loan |

|---|---|---|

| Who can apply | Qualified Pag-IBIG members | Depends on lender rules |

| Basis for approval | Pag-IBIG savings, contributions, records, documents | Income, ID, credit checks, lender policy |

| Loan amount | Based mainly on Pag-IBIG Regular Savings | Based on lender assessment |

| Speed | May require verification | May be faster, depending on lender |

| Cost | Usually more affordable than many short-term private loans | Can have higher interest, fees, or penalties |

| Best for | Members with updated records | Borrowers who are not eligible or need faster access |

| Main risk | Delay if records or documents are incomplete | High total repayment cost if terms are not checked |

If you are considering a private online loan, check the lender’s registration, interest, fees, penalties, repayment schedule, and total repayment amount before applying.

If you are not qualified for a Pag-IBIG loan, you still have options. The right choice depends on why you were not approved.

Continue paying Pag-IBIG contributions and wait until you meet the required savings record.

Prepare the missing documents and reapply only after correcting the issue.

Update your Pag-IBIG member record before submitting another loan application.

Check your outstanding balance, missed payments, or default status. You may need to settle or update your loan before applying again.

Consider other legal options, such as:

Do not borrow from unregistered lenders or loan sharks. Fast cash can become a bigger problem if the interest, penalties, or collection practices are abusive.

Before applying for a Pag-IBIG loan, avoid these mistakes:

Use this checklist before submitting your Pag-IBIG loan application:

A Pag-IBIG loan is a loan program for qualified Pag-IBIG Fund members. The most common cash loan is the Multi-Purpose Loan, but Pag-IBIG also offers Calamity Loan and Housing Loan.

Many Filipinos call it “Pag-IBIG salary loan,” but the official short-term cash loan is called the Pag-IBIG Multi-Purpose Loan. It can be used for personal expenses, not only salary-related needs.

For the Multi-Purpose Loan, qualified members may borrow up to 90% of their total Pag-IBIG Regular Savings, subject to Pag-IBIG assessment and possible deductions.

Under the enhanced MPL rules, the requirement was reduced to at least 12 monthly savings. Always check the latest Pag-IBIG rules before applying, because requirements may change.

Yes. Eligible members can apply for short-term loans through Virtual Pag-IBIG. The online requirements include a loan application form, one valid ID, cash card, and selfie photo showing the ID and cash card.

You can check your status through Virtual Pag-IBIG Loan Status Verification. The page lets users select Housing Loan, Multi-Purpose Loan, or Calamity Loan.

It depends on your loan status and Pag-IBIG’s assessment. If you have an unpaid or defaulted loan, your application may be rejected or delayed. If your existing loan is updated, your outstanding balance may reduce the net proceeds.

Processing time varies. It may depend on your application channel, document completeness, employer validation, loan type, and whether your records need correction. Do not assume that all applications are processed within the same number of days.

Common reasons include insufficient contributions, inactive membership, incomplete documents, mismatched records, unclear ID photos, wrong loan type, employer validation issues, or a defaulted existing Pag-IBIG loan.

Use the official Pag-IBIG website or Virtual Pag-IBIG to get the correct loan form. Avoid old forms from random websites because outdated forms may cause delays.

Yes, OFWs may apply if they are qualified Pag-IBIG members and meet the required savings, contribution, document, and account conditions. They should check Virtual Pag-IBIG or official Pag-IBIG channels for the correct filing process.

First, find out why you are not eligible. If the issue is contributions, documents, or record mismatch, correct it before reapplying. If you need another option, compare SSS loans, employer loans, bank personal loans, or licensed online lenders. Always check the total repayment amount before borrowing.

Interest |

Loan amount |

Term |

Borrower age |

SEC registered |

||

|---|---|---|---|---|---|---|

|

|

APR 145%

|

₱500 — ₱20,000

|

from 3 to 6 months

|

22+ years

|

SEC Registration number: CS201953O73., Certificate of Authority №1254

|

|

|

|

from 0%

|

₱1,000 — ₱50,000

|

up to 12 months

|

20 — 70 years

|

SEC Registration No. CS201908275 SEC Certificate of Authority No. 2990

|

|

|

|

APR 182%

|

₱1,000 — ₱30,000

|

from 7 days to 6 months

|

21 — 70 years

|

SEC Registration No. 2021030009095-02 Certificate of Authority N o. 3427

|

|